Legal recognition & rights

Legal recognition & rights Unlock exclusive July discounts! Enjoy no-cost EMI and limited-time offers on your first purchase.

Get access to July offers!

Offers & discounts just for you.

Ready to Register for GST?

Get your GST registered at myHQ's provided premium addresses

Why should you get GST registration in India?

Legal recognition & rights Input tax credit Business expansion Need a government-compliant office address for GST? Get a Virtual Office starting at ₹799/month

GST registration for popular business structures in India

Private Limited Company (Pvt. Ltd.)

Ideal for service-based businesses Suitable for raising capital through equity Preferred by businesses seeking external investment Separate legal identity from owners Best suited for structured, long-term growth Limited Liability Partnership (LLP)

Ideal for professional services Flexible capital contribution by partners Limited liability with shared responsibilities Governed by a partnership agreement Suitable for jointly managed businesses One Person Company (OPC)

Ideal for freelancers and small-scale businesses Minimal compliance requirements Single-owner structure Full control over business decisions Recognised as a corporate entity

myHQ Assured

Pre-requisite for GST registration in India

Trusted by

Everything you need to have in place before GST registration in India.

Step 1

Finalise your GST Address

Confirm your GST address for your company and gather all required documents

GST Registration in India: A Complete Step-by-Step Guide (2026)

GST registration is the formal process through which a business enrolls under the Goods and Services Tax framework and obtains a unique 15-digit Goods and Services Tax Identification Number (GSTIN). Once registered, the entity can legally collect GST from customers, claim Input Tax Credit (ITC) on eligible purchases, and file returns with the tax authorities.

The GST framework is governed by the Central Goods and Services Tax Act, 2017 (CGST Act) and the respective State GST Acts. The Central Board of Indirect Taxes and Customs (CBIC), under the Ministry of Finance, administers the registration process through the unified portal at gst.gov.in .

GST replaced a fragmented system of indirect taxes including Central Excise Duty, Service Tax, Value Added Tax (VAT), and Central Sales Tax, with a single unified tax framework effective from July 1, 2017. The GST Council, constituted under Article 279A of the Constitution of India, governs rate changes, exemptions, and policy decisions.

Without a valid GSTIN, a business cannot legally charge GST on invoices, claim ITC on input purchases, or undertake inter-state supply in most trade categories.

This guide covers the complete GST registration process applicable across all business structures, including Private Limited Companies, LLPs, OPCs, partnership firms, and proprietorships. For structure-specific documentation requirements, refer to the dedicated guides linked within each relevant section.

Table of contents

Table of contents

Who must register for GST?

Turnover-Based Mandatory Registration

Under Section 22 of the CGST Act, 2017, GST registration is mandatory once aggregate annual turnover crosses the following thresholds:

| Business Type | General States | Special Category States |

|---|---|---|

| Suppliers of Goods | Rs. 40 lakh | Rs. 20 lakh |

| Suppliers of Services | Rs. 20 lakh | Rs. 10 lakh |

The Rs. 40 lakh threshold for goods was introduced via Notification No. 10/2019-Central Tax dated March 7, 2019. Special category states include Manipur, Mizoram, Nagaland, Tripura, Meghalaya, Sikkim, Arunachal Pradesh, Uttarakhand, and Himachal Pradesh.

Mandatory Registration Regardless of Turnover

Under Section 24 of the CGST Act, the following categories must register irrespective of turnover:

- Businesses engaged in inter-state supply of goods must register irrespective of turnover. Interstate service providers are exempt from mandatory registration up to the standard threshold limit under Notification No. 10/2017-Integrated Tax.

- E-commerce operators and sellers supplying through platforms such as Amazon, Flipkart, or Meesho

- Casual taxable persons supplying in a state where they have no fixed place of business

- Non-resident taxable persons supplying goods or services in India

- Persons liable to pay GST under the Reverse Charge Mechanism under Section 9(3) or 9(4) of the CGST Act

- Input Service Distributors (ISD) distributing ITC among branches

- Entities required to deduct TDS under Section 51 of the CGST Act

Voluntary Registration

A business below the threshold may register voluntarily under Section 25(3) of the CGST Act. This is advisable for businesses supplying to registered clients who require ITC-eligible invoices, or those planning inter-state expansion. Once voluntarily registered, a business cannot de-register before one year from the effective registration date, per the proviso to Section 29(1) of the CGST Act.

Types of GST registration

Regular Taxpayer: Standard category for businesses with a fixed place of business. Eligible for full ITC claims and subject to monthly or quarterly return filing.

Composition Scheme Taxpayer: Available for businesses with aggregate turnover below Rs. 1.5 crore (Rs. 75 lakh for specified special category states) under Section 10 of the CGST Act. Composition dealers pay GST at a fixed rate on turnover, cannot collect GST from customers, and cannot claim ITC.

Casual Taxable Person: For businesses without a fixed place of business in a state, supplying taxable goods or services occasionally. Registration is valid for 90 days and requires an advance deposit of estimated tax liability.

Non-Resident Taxable Person: For foreign businesses supplying taxable goods or services in India without a fixed establishment. Registration is valid for 90 days.

Input Service Distributor (ISD): For businesses receiving invoices for input services used across multiple branches and distributing ITC among them.

Documents required for GST registration

- PAN card of the entity or individual

- Aadhaar card of the authorised signatory, proprietor, partners, or directors

- Passport-size photograph of the authorised signatory

- Bank account proof: cancelled cheque or bank statement showing account number, IFSC code, and branch name

Proof of Principal Place of Business (Updated per CBIC Instruction No. 03/2025-GST)

| Premises Type | Required Documents |

|---|---|

| Owned | Any one of: property tax receipt, municipal khata copy, or electricity bill (not older than 2 months) |

| Rented with Registered Agreement | Rent or lease agreement plus any one ownership proof of the lessor. Lessor's PAN or Aadhaar is not required. |

| Rented without Registered Agreement | Rent or lease agreement, ownership proof of lessor, and identity proof of lessor |

| Consent or Shared Premises | Consent letter from the owner, identity proof of the owner, and any one ownership document |

| No Agreement (Relative's or Shared Premises) | Affidavit before a First-Class Judicial Magistrate, Executive Magistrate, or Notary Public, plus one ownership proof |

| SEZ Premises | GST registration certificate or SEZ documents issued by the Government of India |

Under Instruction No. 03/2025-GST, officers are prohibited from requesting the lessor's PAN or Aadhaar, raising queries on presumptive grounds, or demanding documents beyond the prescribed list without prior approval from the Deputy Commissioner or Assistant Commissioner.

Additional Documents by Business Structure

Sole Proprietorship: PAN and Aadhaar of the proprietor, photograph, proof of premises, and bank account details.

Partnership Firm: PAN of the firm, partnership deed, PAN and Aadhaar of all partners, photographs, proof of premises, and bank account details. No Udyam certificate, MSME certificate, or trade licence is required per Instruction No. 03/2025-GST.

Private Limited Company, LLP, OPC, and Other Registered Entities: Certificate of Incorporation, PAN of the entity, PAN and Aadhaar of all directors or designated partners, board resolution authorising the signatory, Digital Signature Certificate (DSC) of the authorised signatory (mandatory for companies and LLPs), proof of premises, and bank account details.

Step-by-step GST registration process (2026)

GST registration is conducted entirely online through gst.gov.in. There is no government fee for GST registration.

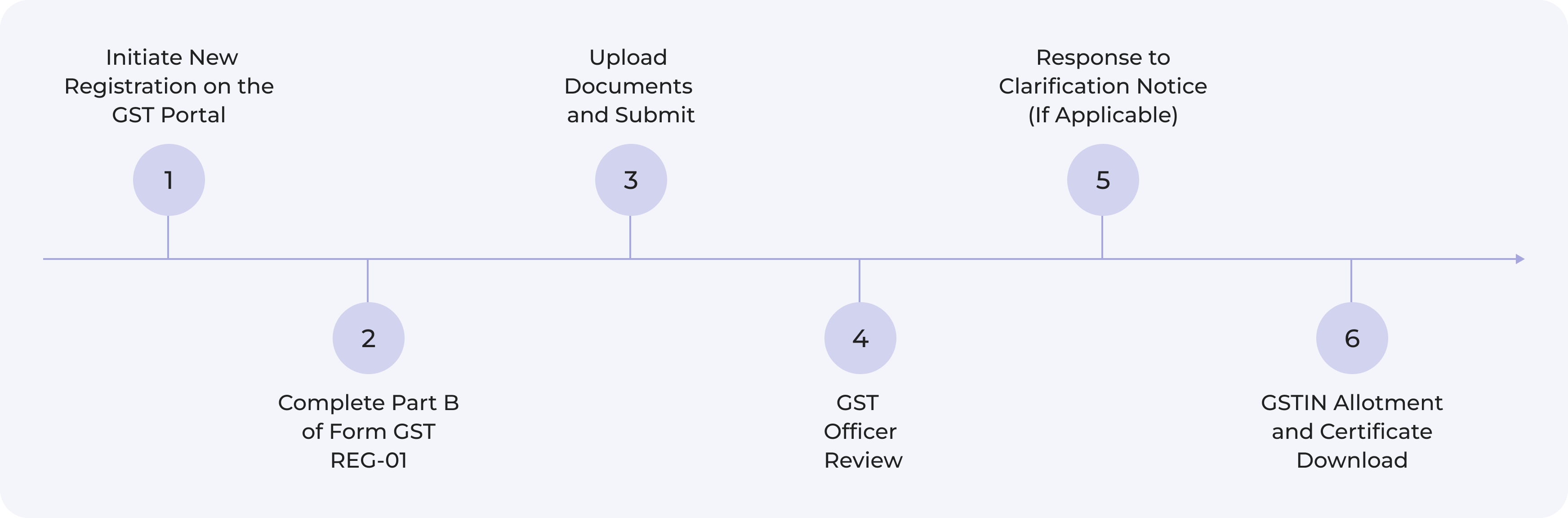

Step 1: Initiate New Registration on the GST Portal

Visit gst.gov.in and navigate to Services > Registration > New Registration. Under the I am a dropdown, select Taxpayer. Select the relevant state and district. Enter the legal name of the business as per the PAN database, the business PAN, and the mobile number and email of the authorised signatory.

An OTP is sent to both the registered mobile and email. Upon successful verification, a Temporary Reference Number (TRN) is generated, valid for 15 days, to be used for completing Part B of the application.

Step 2: Complete Part B of Form GST REG-01

Log in with the TRN and complete the detailed application covering:

Business Details: Trade name, constitution of business, date of commencement, and reason for registration.

Promoters, Partners, or Directors: Name, PAN, Aadhaar, DIN (for company directors), date of birth, designation, and contact details. Photographs must be in JPG format under 100 KB.

Principal Place of Business: Full address including PIN code, district, and jurisdiction details. Select the nature of possession and upload the relevant premises proof per the document table above.

Goods and Services: HSN codes for goods and SAC codes for services. A maximum of five HSN and five SAC codes may be added at registration. Correct classification determines applicable GST rates and return types.

Bank Account Details: Account number, IFSC code, and branch name. For companies and LLPs, the account must be in the name of the entity, not individual directors or partners.

Aadhaar Authentication: If the authorised signatory completes Aadhaar OTP authentication, physical verification of the premises is generally not required. If authentication is declined, physical verification may be initiated by the jurisdictional officer.

Step 3: Upload Documents and Submit

Upload all required documents in PDF or JPG format, with each file not exceeding 1 MB. All document details must be consistent with information entered in the form. Mismatches are a primary cause of clarification notices and delays.

Submit using:

- DSC of the authorised signatory for companies and LLPs

- Electronic Verification Code (EVC) via Aadhaar OTP for all other entity types

Upon submission, an Application Reference Number (ARN) is generated and sent to the registered mobile and email. Application status can be tracked at Services > Registration > Track Application Status on the GST portal.

Step 4: GST Officer Review

The application is reviewed by the jurisdictional GST officer. Processing timelines under the updated framework are:

| Application Category | Processing Timeline |

|---|---|

| Aadhaar-authenticated, standard application | 7 working days from ARN date |

| Non-Aadhaar or high-risk, requiring physical verification | 30 working days from ARN date |

| Automatic electronic registration under Rule 9A (w.e.f. November 1, 2025) | 3 working days |

Rule 9A and Rule 14A were introduced via CBIC Notification No. 18/2025 dated October 31, 2025, under the Central Goods and Services Tax (Fourth Amendment) Rules, 2025. Rule 14A offers simplified electronic registration for businesses with monthly output tax liability to registered persons not exceeding Rs. 2.5 lakh.

Step 5: Response to Clarification Notice (If Applicable)

If the GST officer requires clarification, a notice is issued in Form GST REG-03. The applicant has 7 working days to respond in Form GST REG-04. If no response is received, the officer may reject the application in Form GST REG-05. Officers must obtain prior approval from the Deputy Commissioner or Assistant Commissioner before requesting any document not listed in Form GST REG-01.

Step 6: GSTIN Allotment and Certificate Download

Upon approval, a GSTIN is allotted and a GST Registration Certificate is issued in Form GST REG-06. It is downloadable from Services > User Services > View/Download Certificate on the GST portal.

The GSTIN follows this structure: state code (2 digits) + PAN of the taxpayer (10 digits) + entity count for that PAN in the state (1 digit) + default character Z (1 digit) + check digit (1 digit).

The registration certificate must be displayed at the principal place of business and all additional places of business.

How Virtual Offices support your GST registration?

A valid principal place of business address is mandatory under the CGST Act, 2017. For startups, remote founders, and businesses expanding into new cities, committing to a commercial lease solely for GST registration is neither practical nor cost-effective.

For businesses that do not have a dedicated commercial premise, a Virtual Office address for GST registration is a legally compliant alternative, provided it meets the PPOB documentation requirements under CBIC Instruction No. 03/2025-GST.

myHQ Virtual Office provides a GST-compliant business address across 34+ cities in India, supported by 150+ partner spaces, 50+ Virtual Office Experts, and 10,000+ clients served.

- Digital KYC and Agreement: Complete onboarding online without a physical visit, ideal for founders registering from any location in India.

- Fastest Document Turnaround Time: Rent agreement and NOC documents are delivered promptly so ARN generation is not delayed.

- Flexible Contract Tenures: No long-term lease commitment, suited for early-stage businesses and those requiring multi-state GST registrations.

- Comprehensive Help and Support: Expert guidance on PPOB documentation, officer queries, and clarification notices related to the registered address.

Post-registration compliance obligations

GST Return Filing: Regular taxpayers must file GSTR-1 (outward supplies) by the 11th of the following month for monthly filers or the 13th of the month after the quarter for QRMP filers. GSTR-3B (summary return and tax payment) is due by the 20th for monthly filers, and the 22nd or 24th for QRMP filers depending on the state. The annual return GSTR-9 is due by December 31 of the subsequent financial year.

E-Invoicing: Mandatory for businesses with Annual Aggregate Turnover exceeding Rs. 5 crore. B2B invoices must be uploaded to the Invoice Registration Portal (IRP) to obtain an Invoice Reference Number (IRN) and QR code before issuance to the recipient. Invoices issued without an IRN are treated as invalid under the GST framework.

Input Tax Credit Claims: ITC under Section 16 of the CGST Act is claimable only when the supplier has filed their GSTR-1, the credit reflects in the purchaser's auto-populated GSTR-2B, and the supplier has been paid within 180 days of the invoice date.

GST Payment: Tax liability must be deposited into the Electronic Cash Ledger on the GST portal via net banking, debit card, or NEFT/RTGS. ITC from the Electronic Credit Ledger can be set off against output tax liability before any cash payment is made.

Multi-State Registration: A business operating in more than one state must hold a separate GSTIN for each state, with independent return filing obligations for each registration.

Common mistakes to avoid during GST registration

PAN and Legal Name Mismatch: The legal name in the GST application is auto-populated from the PAN database. If PAN records are outdated or differ from the Certificate of Incorporation, the application will be rejected. Verify PAN details on the Income Tax portal before initiating registration.

Wrong Constitution Type: Selecting proprietorship instead of a private limited company, or partnership instead of an LLP, results in mismatched documentation and triggers a clarification notice. The constitution selected must exactly match the legal structure of the entity.

Blurred or Oversized Document Uploads: Each document must be in JPG or PDF format with a maximum file size of 1 MB. Illegible scans or bank documents where the IFSC code is unclear are frequent causes of officer queries and processing delays.

Using a Personal Bank Account for Companies or LLPs: The bank account submitted must be in the name of the entity. A director’s or partner’s personal account triggers a clarification notice and delays GSTIN allotment.

Incorrect HSN or SAC Code Selection: Codes must correspond to the principal goods and services the business deals in. Incorrect classification leads to rate mismatches at the return filing stage and potential ITC disputes.

Not Tracking ARN Status: Clarification notices in Form GST REG-03 carry a strict 7-working-day response window. Applicants who do not monitor the ARN status risk rejection by default, requiring a fresh application.

Penalties for non-compliance

- Operating Without Mandatory Registration: Penalty of 100% of the tax due or Rs. 10,000, whichever is higher, under Section 122 of the CGST Act. Where deliberate tax evasion is established, the penalty extends to 100% of the tax evaded.

- Late Return Filing: Late fee of Rs. 50 per day (Rs. 20 per day for nil returns) under Section 47, plus interest at 18% per annum on outstanding tax under Section 50.

- Non-Issuance or Incorrect Invoice: Penalty of Rs. 10,000 or the tax evaded, whichever is higher, under Section 122(1)(i).

A word from our community.

myHQ has helped 10,000+ clients get their Virtual Office, boosting productivity and driving business growth.

myHQ Team provided great and fast support to us!

Great and fast service We needed an office for the registration of our company. We found Myhq through Google. The myHQ Team provided great and fast support to us. We recommend using the service of MyHQ once and you won't hesitate to use it again and again.

Harshit Arora

Director, Screen stitcheras

Get an address for your company

Stress free registrations guaranteed with myHQ

Get an address for your company

Stress free registrations guaranteed with myHQ

Frequently Asked Questions

Is GST registration mandatory for all businesses in India?

No. It is mandatory only for businesses crossing the applicable turnover threshold, or falling under the Section 24 categories such as inter-state suppliers, e-commerce sellers.

Can a home address be used for GST registration?

Is a virtual office address valid for GST registration?

What is the penalty for not filing GSTR-10 after GST cancellation?

Can a business hold multiple GSTINs in the same state?

What is the difference between CGST, SGST, and IGST?