Legal recognition and rights

Legal recognition and rights Unlock exclusive July discounts! Enjoy no-cost EMI and limited-time offers on your first purchase.

Get access to July offers!

Offers & discounts just for you.

Ready to register GST for your Limited Liability Partnership?

Get your GST registered at myHQ's provided premium addresses

Why should you get GST registration in India?

Legal recognition and rights Input tax credit benefits Easier business expansion Need a government-compliant office address for GST? Get a Virtual Office starting at ₹799/month

myHQ Assured

Prerequisites for GST registration for a LLP in India

Trusted by

Everything you need in place before starting your GST registration

Step 1

Confirm your business address for GST

Provide a valid business address for your LLP. Don’t have one? Use a government-compliant Virtual Office address to complete your GST registration seamlessly

GST Registration for LLP: Step-by-Step Process (2026)

GST registration for a Limited Liability Partnership (LLP) is the process through which the entity obtains a Goods and Services Tax Identification Number (GSTIN) under the Central Goods and Services Tax Act, 2017. A GSTIN authorises the LLP to collect GST on taxable supplies, claim Input Tax Credit (ITC), file periodic returns, and conduct inter-state commerce.

An LLP is a distinct legal entity under the Limited Liability Partnership Act, 2008 . Its GST registration profile differs from sole proprietorships and partnership firms in two key respects: DSC-based submission is mandatory under Rule 26(2) of the CGST Rules, 2017, and the LLP Agreement serves as the primary constitutional document rather than a Memorandum or Articles of Association.

This guide covers the complete GST registration process for LLPs in 2026, incorporating the latest regulatory changes under GST 2.0 and Finance Bill, 2026.

Table of contents

Table of contents

What is a Limited Liability Partnership?

A Limited Liability Partnership (LLP) is a separate legal entity formed by two or more partners, where each partner’s liability is limited to their agreed contribution.

Legal Meaning of LLP Under the LLP Act, 2008

An LLP is recognized as a separate legal entity under the Limited Liability Partnership Act, 2008. Key points include:

- Has a legal identity separate from its partners

- Can own property, enter into contracts, and sue or be sued in its own name

- Limits the liability of partners to their agreed capital contribution

How LLP Is Different From a Traditional Partnership

Unlike a traditional partnership firm, an LLP provides additional legal and operational protections:

- Partners are not personally liable for the misconduct, negligence, or business losses caused by other partners

- The LLP enjoys perpetual succession, continuing to exist even if partners change or exit

- Compliance and registration are governed by the Ministry of Corporate Affairs (MCA), ensuring legal recognition and regulatory oversight

LLPs are governed by the LLP Act, 2008 and registered with the Ministry of Corporate Affairs (MCA).

Is GST registration mandatory for an LLP

Turnover-Based Threshold

Under Section 22 of the CGST Act, 2017, GST registration becomes mandatory for an LLP once its aggregate annual turnover crosses the applicable threshold:

| Supply Type | General States | Special Category States |

|---|---|---|

| Goods | Rs. 40 lakh | Rs. 20 lakh |

| Services | Rs. 20 lakh | Rs. 10 lakh |

Aggregate turnover includes all taxable supplies, exempt supplies, exports, and inter-state supplies across all business verticals under the same PAN. Inward supplies on which GST is payable under Reverse Charge Mechanism (RCM) are excluded from the aggregate turnover calculation.

Special category states include Manipur, Mizoram, Nagaland, Tripura, Meghalaya, Sikkim, Arunachal Pradesh, Uttarakhand, and Himachal Pradesh.

Mandatory Registration Regardless of Turnover

Under Section 24 of the CGST Act, an LLP must register irrespective of turnover if it supplies goods or services across state lines, sells through e-commerce platforms, is liable to pay GST under RCM under Section 9(3) or 9(4), or functions as an Input Service Distributor.

Voluntary Registration

An LLP below the threshold may opt for voluntary registration under Section 25(3) of the CGST Act. This is relevant for LLPs in professional services supplying to GST-registered B2B clients who require ITC-eligible invoices. Once voluntarily registered, cancellation cannot be sought before one year from the effective date, per the proviso to Section 29(1).

How GST applies to an LLP: key tax distinction

For GST purposes, an LLP is treated on par with a company. Both are subject to identical GST registration requirements, including mandatory DSC submission, return filing obligations, and e-invoicing thresholds. LLPs in professional services such as consulting, law, or architecture are service providers and must register once the Rs. 20 lakh turnover threshold is crossed. LLPs in trading or manufacturing follow the Rs. 40 lakh threshold.

Benefits of GST registration for an LLP

Input Tax Credit: A registered LLP can offset GST paid on purchases, professional fees, and capital goods against its output tax liability, reducing the net tax burden on operations.

Inter-State Business: Without a GSTIN, an LLP cannot legally conduct inter-state taxable supply. Registration is a prerequisite for expanding service or product delivery beyond the home state.

Institutional and B2B Credibility: Corporate clients, government procurement processes, and funding institutions require a valid GSTIN as a condition for engagement or empanelment.

E-Commerce Access: LLPs selling through aggregator platforms require GST registration regardless of turnover, making early registration a practical necessity for digitally-distributed businesses.

Budget 2026 Benefit: Post-Supply Discount Flexibility: Under Finance Bill, 2026, Section 15(3)(b) of the CGST Act has been amended to remove the requirement of a pre-existing agreement for post-supply discount deductions. From the notified date (proposed April 1, 2026), LLPs can issue credit notes under Section 34 for discounts without a prior documented agreement, subject to the recipient reversing the related ITC.

Documents required for GST registration of an LLP

The following requirements are based on Form GST REG-01 and CBIC Instruction No. 03/2025-GST dated April 17, 2025.

LLP-Level Documents

- PAN card of the LLP (mandatory; the legal name in the GST application is auto-populated from the PAN database and must match the Certificate of Incorporation)

- Certificate of Incorporation of the LLP issued by the Registrar of Companies under the LLP Act, 2008 (Form 16 issued by the ROC)

- LLP Agreement registered with the Registrar of Companies (filed as Form 3 with the MCA). An unregistered or draft agreement is not accepted.

Designated Partner-Level Documents

- PAN card of the designated partner

- Aadhaar card of the designated partner (must be linked to a mobile number for OTP-based verification during the application)

- Passport-size photograph in JPG format

- DPIN or DIN of each designated partner. DPINs are allotted by the MCA to designated partners under Rule 10 of the LLP Rules, 2009. An individual who holds a DIN from a company directorship does not need a separate DPIN.

Authorised Signatory Documents

- Partners' Resolution or Authorisation Letter naming a specific designated partner as the authorised signatory, signed by all designated partners. This is the LLP equivalent of a board resolution.

- Class 3 DSC of the authorised signatory. Mandatory for LLPs under Rule 26(2) of the CGST Rules, 2017.

Proof of Principal Place of Business

As per CBIC Instruction No. 03/2025-GST:

| Premises Type | Required Documents |

|---|---|

| LLP-owned premises | Any one of: property tax receipt, municipal khata copy, or electricity bill not older than 2 months |

| Rented with registered agreement | Rent or lease agreement plus any one ownership proof of the lessor. Lessor's PAN or Aadhaar is not required. |

| Rented without registered agreement | Rent or lease agreement, ownership proof of lessor, and identity proof of lessor |

| Consent premises (designated partner's residence or third party) | Consent letter from the owner, identity proof of owner, and any one ownership document |

| Virtual office address | Rent or lease agreement from the virtual office provider and NOC. Accepted as valid PPOB under Instruction No. 03/2025-GST, provided the address is a verifiable physical location. |

Bank Account Documents

- Cancelled cheque or bank statement showing the account number, IFSC code, branch name, and the LLP's name. The account must be in the name of the LLP. Under the GSTN Advisory dated November 20, 2025, bank details must be submitted within 30 days of GSTIN allotment or before the first GSTR-1 filing. Non-compliance results in registration suspension and blocking of returns, e-invoicing, and ITC.

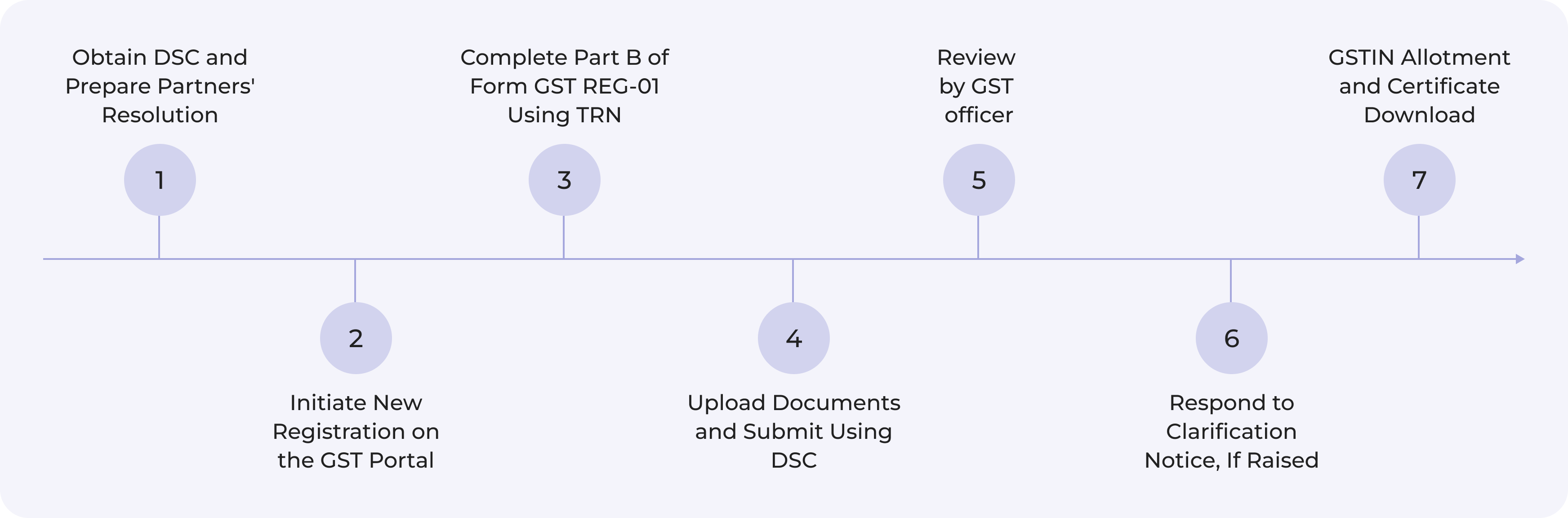

Step-by-step GST registration process for an LLP (2026)

There is no government fee for GST registration. The process is conducted entirely online through gst.gov.in.

Step 1: Obtain DSC and Prepare Partners' Resolution

This step is specific to LLPs and must be completed before initiating the portal application. EVC via Aadhaar OTP is not available for LLPs. The authorised signatory's Class 3 DSC must be obtained from an MCA-authorised Certifying Authority and installed on the filing device. A Class 3 DSC costs approximately Rs. 1,000 to Rs. 3,000 depending on the certifying authority and validity period.

The Partners' Resolution naming the specific designated partner as the GST authorised signatory must be signed by all designated partners and kept ready for upload before the application is initiated.

Step 2: Initiate New Registration on the GST Portal

Visit gst.gov.in and navigate to Services > Registration > New Registration. Select Taxpayer from the I am a dropdown. Select the state and district of the LLP's registered office. Enter the legal name as per PAN, the LLP's PAN, and the mobile number and email of the authorised signatory. An OTP is sent to both contacts. Upon verification, a TRN is generated and remains valid for 15 days.

Step 3: Complete Part B of Form GST REG-01 Using TRN

Log in using the TRN and complete the multi-section application.

Business Details: Select the constitution as LLP. Enter the trade name, date of incorporation, and reason for registration.

Promoters and Designated Partners: Enter name, PAN, Aadhaar, DPIN or DIN, date of birth, residential address, and designation for each designated partner. Photographs must be in JPG format. Each designated partner's Aadhaar must be linked to their mobile for OTP verification.

Authorised Signatory: Enter the details of the designated partner named in the Partners' Resolution. This person's DSC will be used to submit the application.

Principal Place of Business: Enter the complete registered office address, PIN code, district, commissionerate, division, and range code. Use the jurisdiction hyperlink on the portal to identify the correct GST range. Select the nature of possession and upload the corresponding address proof.

Goods and Services: Enter HSN codes for goods and SAC codes for services, up to five of each. LLPs in professional services will primarily use SAC codes. Correct classification determines the applicable GST rate and return type.

Bank Account Details: Enter the account number, IFSC code, and branch name of the LLP's current account. Submit at registration to avoid triggering the 30-day post-registration bank detail obligation under the GSTN Advisory dated November 20, 2025.

Step 4: Upload Documents and Submit Using DSC

Upload all documents in PDF or JPG format with each file not exceeding 1 MB. Before submitting, verify the Certificate of Incorporation name matches the PAN and legal name in the form, the Partners' Resolution names the same individual as the authorised signatory, and the address proof corresponds to the PPOB entered.

Submit using the authorised signatory's Class 3 DSC, pre-registered on the GST portal for the relevant PAN. Upon submission, an ARN is generated and sent to the registered mobile and email. Track status at Services > Registration > Track Application Status.

Step 5: GST Officer Review

The jurisdictional GST officer reviews the application. Processing timelines under the current framework are:

| Application Type | Timeline |

|---|---|

| Aadhaar-authenticated, standard application | 7 working days from ARN date |

| Non-Aadhaar or high-risk (physical verification required) | 30 working days from ARN date |

| Rule 9A automatic electronic registration (w.e.f. November 1, 2025) | 3 working days |

For LLPs, Aadhaar authentication is completed at the designated partner level. If all designated partners complete Aadhaar OTP verification, the application is generally processed within the 7-working-day window. LLPs qualifying under Rule 14A (monthly output tax liability to registered persons not exceeding Rs. 2.5 lakh) benefit from the 3-working-day fast-track pathway.

Step 6: Respond to Clarification Notice, If Raised

If the officer requires clarification, a notice is issued in Form GST REG-03. The LLP has 7 working days to respond in Form GST REG-04. Under CBIC Instruction No. 03/2025-GST, officers must obtain approval from the Deputy Commissioner or Assistant Commissioner before requesting documents not listed in Form GST REG-01. Common triggers in LLP applications include submission of an unregistered LLP Agreement, a PPOB-incorporation address mismatch, or name discrepancies across PAN and Aadhaar records. Non-response within 7 working days results in rejection via Form GST REG-05.

Step 7: GSTIN Allotment and Certificate Download

Upon approval, a 15-digit GSTIN is allotted and a GST Registration Certificate is issued in Form GST REG-06, downloadable from Services > User Services > View/Download Certificate. The GSTIN follows: state code (2 digits) + LLP PAN (10 digits) + entity count for that PAN in the state (1 digit) + default Z + check digit. An LLP in multiple states holds a distinct GSTIN per state with independent filing obligations. The certificate must be displayed at the registered office and all additional places of business.

How myHQ Virtual Offices support GST registration for LLPs

A valid principal place of business address is mandatory under the CGST Act, 2017. For newly incorporated LLPs, professional firms in the pre-revenue stage, or those expanding services to new cities, a full commercial lease solely for registration purposes is an avoidable cost.

myHQ Virtual Office provides GST-compliant registered addresses across 34+ cities in India, supported by 150+ partner spaces, 50+ Virtual Office Experts, and 10,000+ clients served.

- Digital KYC and Agreement: Entire onboarding completed online with no physical visit required, ideal for LLP partners in multiple locations.

- Fastest Document Turnaround Time: Rent agreement and NOC delivered promptly so ARN generation is not delayed.

- Flexible Contract Tenures: No long-term lease commitment, suited for early-stage LLPs and those requiring separate GSTINs across multiple states.

- Comprehensive Help and Support: Dedicated experts guide LLPs through PPOB documentation, officer queries, and REG-03 notices relating to the registered address.

For a detailed walkthrough on using a Virtual Office address for GST registration, refer to GST Registration with a Virtual Office Address.

Union budget 2026 and GST 2.0: what LLPs must know

Post-Supply Discount Deduction (Section 15 and 34 Amendment): Finance Bill, 2026 removes the requirement for a pre-existing agreement before claiming post-supply discount deductions. LLPs can issue credit notes under Section 34 from the notified date (proposed April 1, 2026) without documenting a prior agreement, as long as the recipient reverses the related ITC.

Provisional Refund for Inverted Duty Structure (Section 54 Amendment): The 90% provisional refund facility, previously limited to zero-rated supplies, has been extended to inverted duty structure claims. LLPs in sectors where input GST rates exceed output rates will benefit from improved working capital and faster refunds.

Place of Supply for Intermediary Services: Amendments clarifying place of supply for intermediary services benefit LLPs providing consulting, legal, or IT support services to overseas clients, reducing disputes on whether such supplies qualify as exports.

GST 2.0 and Rule 9A / Rule 14A: Introduced via CBIC Notification No. 18/2025 dated October 31, 2025, the simplified registration framework reduces registration time to 3 working days for eligible LLPs under Rule 14A (monthly output tax liability to registered persons not exceeding Rs. 2.5 lakh). LLPs may also withdraw from the Rule 14A scheme using Form REG-32, as enabled by the GSTN Advisory dated February 21, 2026.

Post-registration compliance for LLPs

GST Return Filing: LLPs with annual aggregate turnover above Rs. 5 crore must file GSTR-1 monthly by the 11th and GSTR-3B by the 20th of the following month. LLPs below Rs. 5 crore may opt for the QRMP scheme with quarterly filing. GSTR-9 (annual return) is due by December 31 of the subsequent financial year. GSTR-9C is mandatory for LLPs exceeding Rs. 5 crore turnover.

E-Invoicing: Mandatory for LLPs with Annual Aggregate Turnover exceeding Rs. 5 crore. All B2B invoices must be uploaded to the Invoice Registration Portal (IRP) to obtain an IRN and QR code. Invoices without an IRN are invalid.

ITC Claims: Under Section 16 of the CGST Act, ITC is claimable only when the credit appears in the LLP's auto-populated GSTR-2B and the supplier has been paid within 180 days of the invoice date.

MCA Annual Compliance: LLPs must also file Form 11 (Annual Return) with the MCA by May 30 and Form 8 (Statement of Account and Solvency) by October 30 each year. GST and MCA compliance run as parallel, independent obligations.

Common mistakes to avoid

Submitting an Unregistered LLP Agreement: The LLP Agreement uploaded must be the ROC-registered Form 3 version. A draft or unstamped agreement is not accepted and is a primary REG-03 trigger.

DSC Not Pre-Registered on the Portal: The authorised signatory's Class 3 DSC must be registered on the GST portal before submission. Attempting to submit without it causes application failure.

Partners' Resolution Naming a Different Signatory: The designated partner named in the resolution and the authorised signatory in the form must be the same individual. Any mismatch triggers a clarification notice.

LLP PAN Used in Designated Partner Fields: Partner detail fields require each designated partner's individual PAN, not the LLP PAN. This causes a mismatch with the MCA database.

Not Submitting Bank Details Within 30 Days: Under the GSTN Advisory dated November 20, 2025, failure to submit bank details within 30 days of GSTIN allotment results in suspension, blocking return filing and ITC.

A word from our community.

myHQ has helped 10,000+ clients get their Virtual Office, boosting productivity and driving business growth.

myHQ Team provided great and fast support to us!

Great and fast service We needed an office for the registration of our company. We found Myhq through Google. The myHQ Team provided great and fast support to us. We recommend using the service of MyHQ once and you won't hesitate to use it again and again.

Harshit Arora

Director, Screen stitcheras

Get an address for your company

Stress free registrations guaranteed with myHQ

Get an address for your company

Stress free registrations guaranteed with myHQ

Frequently Asked Questions

Is DSC mandatory for an LLP to register for GST?

Yes. Under Rule 26(2) of the CGST Rules, 2017, DSC-based submission is mandatory for LLPs. Aadhaar OTP-based EVC, available for proprietorships and partnership firms, cannot be used by LLPs.

Can a designated partner's residential address be used as the PPOB?

What is the difference between a DPIN and DIN for GST purposes?

How many GSTINs does an LLP need if it operates in multiple states?

What is the penalty for operating without mandatory GST registration?